News

RipplesMetrics: Nigeria ranks 10th in non-performing loans, as micro-finance banks write off N7.35bn bad debts in 5 years

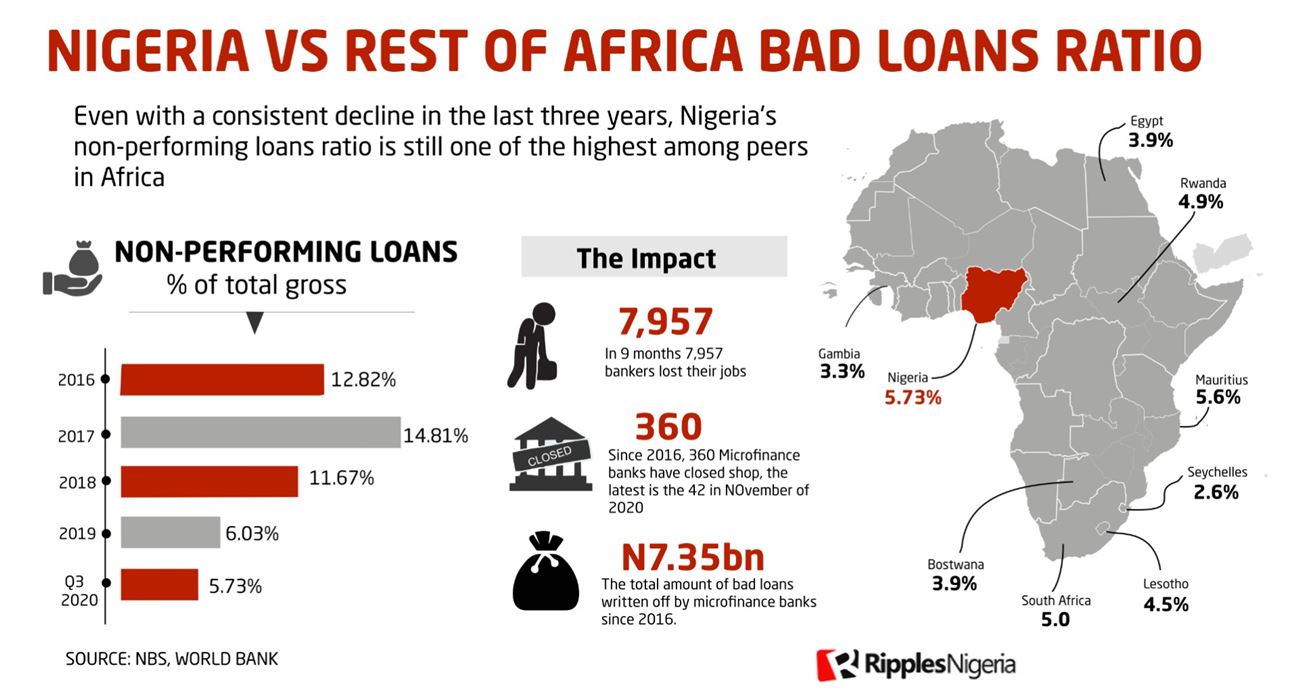

Even with a consistent decline in the last three years, Nigeria’s non-performing loans ratio is still one of the highest among peers in Africa at 10th place.

The latest banking data published by the National Bureau of Statistics (NBS) reveal that out of the N19.46 trillion loans given out to customers in the third quarter, 5.73 per cent which is N1.16 trillion is in default, a figure higher than nine other African countries.

South Africa, Africa’s second largest economy, has a non-performing loan ratio of 5 per cent as at September 2020; Egypt, 3.9 percent as at June 2020; Botswana, 3.9 per cent; Lesotho, 4.5 percent; Gambia, 3.3 percent; Mauritius, 5.6 percent; Seychelles, 2.6%; Rwanda, 4.9 per cent; and, Uganda, 5.7 per cent.

Nigeria’s figure, however, is lower than that of countries like Kenya, whose non-performing loan ratio stood at 15.9% as at June 2020 and Ghana 15.8%, as at September 2020.

A non-performing loan (NPL) or bad loans are debts that have received no scheduled payment in over 90 days, hence regarded as default.

Since 2017, there has been a significant drop of banks’ bad loans from 14.81 percent in 2017, 11.6 percent in 2018 to 6.03 percent in 2019.

The Impact

Though data from NBS show a demonstrable positive momentum from CBN in bad debts recovery, the numbers, however, show that bad debts are still off their lowest in December 2014 when they stood at 2.9 per cent against the recommended 5.0 per cent prudential requirement for a healthy banking sector.

A further analysis of the figures from NBS shows that bad loans recovery hasn’t yet staved off on microfinance banks that serve micro-entrepreneurs and low-income households as there is a 199.8 per cent increase of bad loans from N125 million in first quarter to N377 million in third quarter.

It becomes even more worrisome, as the data also revealed that over N7.35 billion bad loans had been written off in five years, with 318 microfinance banks closing shops in three.

Just last month (November, 2020), another 42 microfinance banks were liquidated as part of series of clean up by the two banking regulators NDIC and CBN.

“Most MFBs have been battling with high level of non-performing loans which had inevitably resulted in high portfolio risk (PAR) which impaired their capital and liquidity to do businesses. With Nigeria contributing the most with 6.6 million to the rise in global poverty, it even becomes scarier,” Omobola Kunle a research analyst explained.

Victor Opara, an economist, further explained that huge bad loans are the bane and nightmare of most banks.

“It is on record that most large banks that went under in the past was a result of humongous toxic loans in their books, which largely squeeze their ability to meet depositors obligation as at when due”

What next?

According to available research, countries with low non-performing loan ratio tend to experience faster GDP growth rate. Non-performing loans decrease banks’ willingness and ability to lend as the banks tend to spend time looking to recover on such loans than making new loans.

This creates yet another problem because bank lending is a catalyst for economic development, so much that, a credit crunch arising from banks’ unwillingness to lend due to non-performing loans can create more of such non-performing loans if the needed economic growth and development is not realized because of such credit crunch.

With Asset Management Corporation of Nigeria (AMCON), which was established to help buy bad loans and salvage the industry from collapse following the financial crisis of 2009, winding up by 2023, it is important CBN continues on the momentum to address this issue of non-performing loans.

By Dave Ibemere…

Join the conversation

Support Ripples Nigeria, hold up solutions journalism

Balanced, fearless journalism driven by data comes at huge financial costs.

As a media platform, we hold leadership accountable and will not trade the right to press freedom and free speech for a piece of cake.

If you like what we do, and are ready to uphold solutions journalism, kindly donate to the Ripples Nigeria cause.

Your support would help to ensure that citizens and institutions continue to have free access to credible and reliable information for societal development.

German Police bust alleged Nigerian scam dating ring

German authorities have arrested eleven individuals suspected of being members of a Nigerian mafia group involved in a large-scale dating...

INVESTIGATION: In Kwara, multimillion-naira milk processing plant is abandoned, converted to a chicken outlet

After the government spent millions of naira to establish a milk processing plant in Kwara State that would provided jobs...

SPECIAL REPORT: For Sokoto communities, promise of healthcare is akin to death sentence

In this story, ABDULRASHEED HAMMAD delves into the dire realities of Primary Health Care services in Sokoto State, shedding light...

ICYMI…SPECIAL REPORT: NNPCL hides behind PIA to frustrate disclosure, accountability

Nigeria’s major oil company, Nigerian National Petroleum Corporation Limited (NNPCL), in what appears to be a common practice of disregard...

INVESTIGATION: Multi-million naira Ekiti resort center remains uncompleted a decade after

The multimillion-naira project, expected to comprise recreational buildings, now consists of cassava farmland, a bush used for excretion, and a...